Unlevering the Equity Cost of Capital-Low Leverage & High Leverage Companies: Below, we show the information for two potential comparable companies. Calculate the unlevered cost of capital based on the following assumptions. Neither company expects its free cash flows to grow. Income tax rate for interest (TINT) Value of debt Value of preferred stock. Value of equity Maturity of debt (years) Debt cost of capital Preferred stock cost of capital. Equity cost of capital Low Leverage Company 35.0% $ 4,000 $ 1,000 $15,000 Perpetual 5.0% 6.0% 11.8% High Leverage Company 45.0% $45,000 $ 0 $ 5,000 Perpetual 8.0% 28.0% a. b. Assume that interest is tax deductible and that the discount rate for all interest tax shields is the unlevered cost of capital. Assume that interest is tax deductible and that the discount rate for all interest tax shields is the cost of debt. C. Assume that interest is tax deductible but that the company refinances its debt at the end of each year (annual refinancing).

Unlevering the Equity Cost of Capital-Low Leverage & High Leverage Companies: Below, we show the information for two potential comparable companies. Calculate the unlevered cost of capital based on the following assumptions. Neither company expects its free cash flows to grow. Income tax rate for interest (TINT) Value of debt Value of preferred stock. Value of equity Maturity of debt (years) Debt cost of capital Preferred stock cost of capital. Equity cost of capital Low Leverage Company 35.0% $ 4,000 $ 1,000 $15,000 Perpetual 5.0% 6.0% 11.8% High Leverage Company 45.0% $45,000 $ 0 $ 5,000 Perpetual 8.0% 28.0% a. b. Assume that interest is tax deductible and that the discount rate for all interest tax shields is the unlevered cost of capital. Assume that interest is tax deductible and that the discount rate for all interest tax shields is the cost of debt. C. Assume that interest is tax deductible but that the company refinances its debt at the end of each year (annual refinancing).

Fundamentals of Financial Management, Concise Edition (with Thomson ONE - Business School Edition, 1 term (6 months) Printed Access Card) (MindTap Course List)

8th Edition

ISBN:9781285065137

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Eugene F. Brigham, Joel F. Houston

Chapter13: Capital Structure And Leverage

Section: Chapter Questions

Problem 14SP: WACC AND OPTIMAL CAPITAL STRUCTURE Elliott Athletics is trying to determine its optimal capital...

Related questions

Question

Transcribed Image Text:6

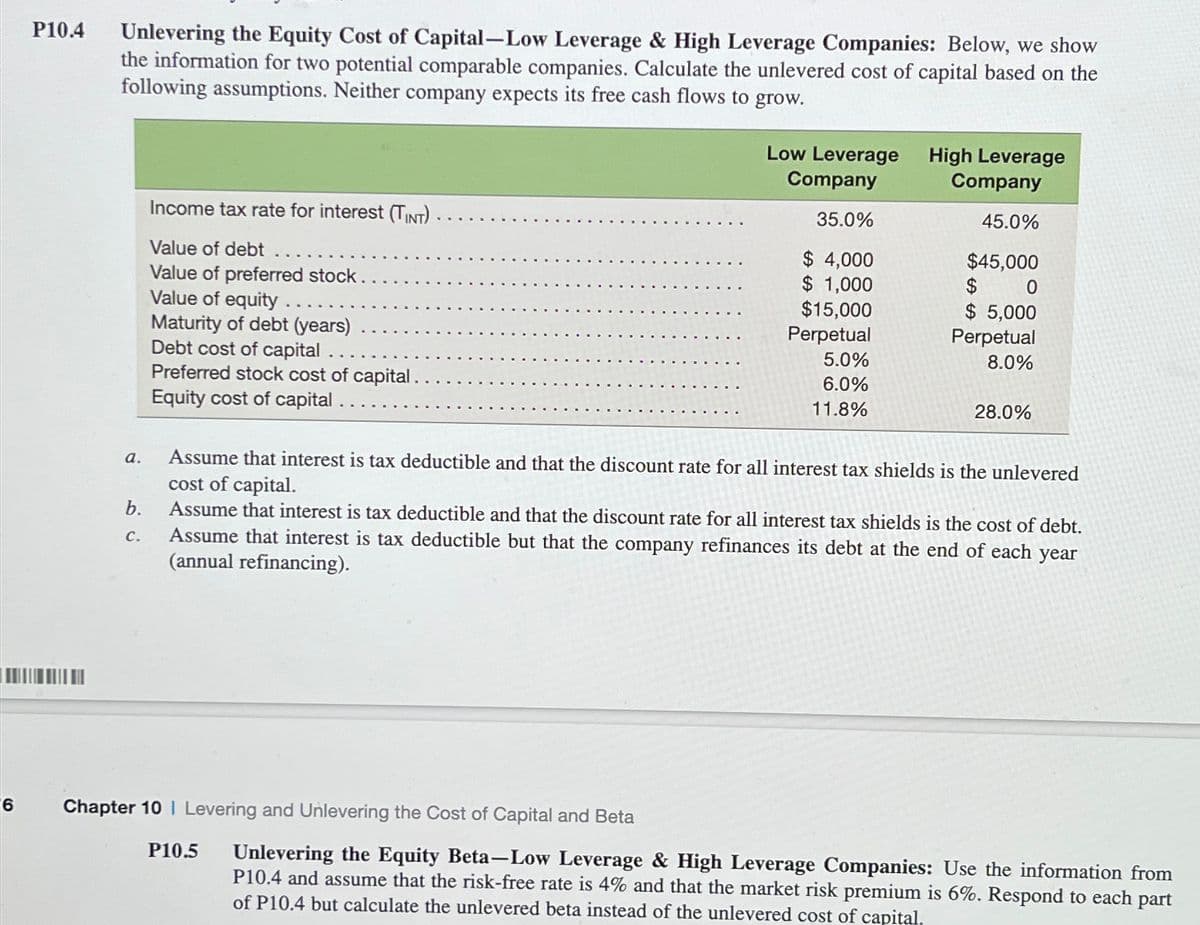

P10.4

Unlevering the Equity Cost of Capital-Low Leverage & High Leverage Companies: Below, we show

the information for two potential comparable companies. Calculate the unlevered cost of capital based on the

following assumptions. Neither company expects its free cash flows to grow.

Income tax rate for interest (TINT).

Value of debt

Value of preferred stock.

Value of equity

Maturity of debt (years)

Debt cost of capital.

Preferred stock cost of capital.

Equity cost of capital.

Low Leverage

Company

High Leverage

Company

35.0%

$ 4,000

$ 1,000

$15,000

45.0%

$45,000

$

0

Perpetual

$ 5,000

Perpetual

5.0%

8.0%

6.0%

11.8%

28.0%

a.

b.

C.

Assume that interest is tax deductible and that the discount rate for all interest tax shields is the unlevered

cost of capital.

Assume that interest is tax deductible and that the discount rate for all interest tax shields is the cost of debt.

Assume that interest is tax deductible but that the company refinances its debt at the end of each year

(annual refinancing).

Chapter 10 | Levering and Unlevering the Cost of Capital and Beta

P10.5

Unlevering the Equity Beta-Low Leverage & High Leverage Companies: Use the information from

P10.4 and assume that the risk-free rate is 4% and that the market risk premium is 6%. Respond to each part

of P10.4 but calculate the unlevered beta instead of the unlevered cost of capital.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 5 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781285065137

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781305635937

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781285065137

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781305635937

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning