Videos

Subsequent events

• LO13–6

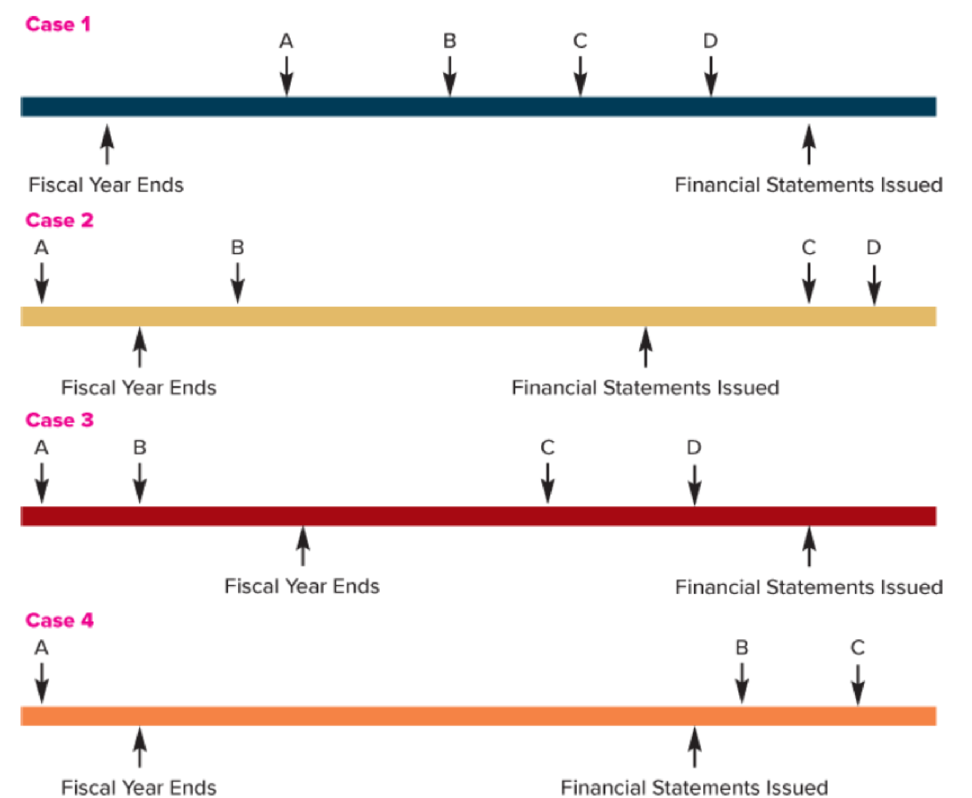

Lincoln Chemicals became involved in investigations by the U.S. Environmental Protection Agency in regard to damages connected to waste disposal sites. Below are four possibilities regarding the timing of (A) the alleged damage caused by Lincoln, (B) an investigation by the EPA, (C) the EPA assessment of penalties, and (D) ultimate settlement. In each case, assume that Lincoln is unaware of any problem until an investigation is begun. Also assume that once the EPA investigation begins, it is probable that a damage assessment will ensue and that once an assessment is made by the EPA, it is reasonably possible that a determinable amount will be paid by Lincoln.

Required:

For each case, decide whether (1) a loss should be accrued in the financial statements with an explanatory note, (2) a disclosure note only should be provided, or (3) no disclosure is necessary.

Want to see the full answer?

Check out a sample textbook solution

Chapter 13 Solutions

Intermediate Accounting

- Q21 Which of the following is NOT a step in impairment testing? Select one: a. Sell the asset after if the fair value is greater than the recoverable amount b. Calculate the asset’s carrying amount in the books of the entity c. Calculate the recoverable amount of the asset d. Assess whether there are circumstances that may indicate that the asset should be impaired.arrow_forwardQ23 Which of the following statement(s) is (are) true? (i) An intangible asset is impaired if the carrying amount is higher than its recoverable amount (ii) Recoverable amount is the asset’s fair value or its value-in-use at the reporting date. (iii) For an intangible asset with infinite useful life, impairment test should be performed only if there is evidence to indicate that an intangible asset has been impaired. (iv) For an intangible asset with finite useful life, impairment test should be performed annually even if there is no evidence that the asset has been impaired. Select one: a. (i), (ii), (iii) and (iv) b. (i) and (ii) only c. (i) and (iv) only d. (i) onlyarrow_forwardIn the U.S. courts, those seeking to be compensated for damages due to environmental pollution must demonstrate that the emissions at issue caused the damages that are 1) presented. 2) demonstrate that the emissions at issue came from the specific defendant. 3) file an action within a specified period of time (typically 2-3 years). 4) all of the above.arrow_forward

- ! Required Information Ch06 Predecessor-Successor Auditor Communications [LO6-2] Predecessor-Successor Auditor Communications Read the case, then answer the questions that follow. Audit standards require successor auditors to attempt to communicate with the predecessor before accepting an audit engagement. CONCEPT REVIEW: Audit standards require successor auditors to attempt communication with the predecessor auditors. The predecessors must have permission from the previous client before sharing Information with the successor auditors. Predecessor auditors will help successor auditors to determine whether or not to accept an engagement. Part 2 - Concept Check 1. Successor auditors need to communicate with predecessor auditors. 2. accepting the engagement. must ask management to authorize the predecessor auditors to discuss confidential information. 3. If predecessor auditors refuse communication, successor auditors accept the engagement. 4. Communication between predecessor and…arrow_forward4G+ 12:16 PM O 0.1KB/s O 68 00:43:39 Remaining Multiple Choice Which of the following statements is false regarding RESEARCH and DEVELOPMENT (R&D) COSTS? RESEARCH activities are undertaken to discover new knowledge that will be useful in developing new product or in significantly improving an existing product. O DEVELOPMENT activities involve the application of research findings to develop a new product prior to the start of commercial production. No intangible asset arising from research shall be recognized; expenditure on research shall be recognized as an expense when it is incurred. If an entity cannot distinguish the research phase from the development phase, the entity treats the R&D expenditure as if it were incurred in the development phase only 11 of 25 レarrow_forward4G+ 12:47 PM 0.4KB/s ill 68 וח 01:14:08 Remaining Multiple Choice Which statement is incorrect with respect to depreciation? Depreciation is not recognized if the fair value of an asset exceeds carrying amount. Depreciation ceases at the earlier between the date the asset is classified as held for sale and the date the asset is derecognized. The depreciation method shall reflect the pattern in which the asset's economic benefits are consumed by the entity. Depreciation of an asset begins when it is available for use or when it is in the location and condition necessary for the intended use. 45 of 75arrow_forward

- #32 of 20 questions Multiple Choices --Previous Questions-- Multiple Choice Questions The following are risks of ownership Except: OLessee maintained assets OLessee has right to use assets for most or all of it useful life. OLessee runs the risk of technological obsolescence. b) Lessee insures assets OLessee insures asset dyarrow_forwardS8 The term inadequacy refers to: Multiple Choice The inability of a plant asset to meet its demands. An asset reaching its book value. An asset that does not have a salvage value. The condition where the salvage value is too small to replace the asset. The process of depletion.arrow_forwardEx 17.3 Joining Ltd has acquired a license to explore an area of interest and wants to capitalise its Exploration and Evaluation (E&E)expenditures on an area of interest basis.The following costs have been incurred .Required:Which costs can be capitalised as E & E assets under AASB 6?(a) the acquisition of speculative seismic data in relation to the area of interest to help determine whether to apply for an exploration licence (b)labour costs of engineers analysing the seismic data(c)the exploration licence fee(d)legal costs of obtaining the exploration licence(e)labour costs for engineers to carry out topographical,geological and geophysical studies on the area after exploration licence obtained(f)payroll costs related to the engineering costs(g)contractors fees for exploratory drilling(h)hire fees for drilling equipmentarrow_forward

- 10. Which of the following statement is false? The cost of an internally generated patent is confined to legal and registration fees only An intangible asset with definite life is amortized Goodwill is an intangible asset but not under PAS 38 The cost of modification of a product to conform with customer's demand is an R&D expensearrow_forward(Loss Contingency) Presented below is a note disclosure for Matsui Corporation. Litigation and Environmental: The Company has been notified, or is a named or a potentially responsible party in a number of governmental (federal, state and local) and private actions associated with environmental matters, such as those relating to hazardous wastes, including certain sites which are on the United States EPA National Priorities List (“Superfund”). These actions seek clean-up costs, penalties and/or damages for personal injury or to property or natural resources.In 2017, the Company recorded a pre-tax charge of $56,229,000, included in the “Other expense (income)—net” caption of the Company’s consolidated income statements, as an additional provision for environmental matters. These expenditures are expected to take place over the next several years and are indicative of the Company’s commitment to improve and maintain the environment in which it operates. At December 31, 2017, environmental…arrow_forwardQuestion # 10 a. Over what period of time should the cost of a patent acquired by purchased be amortized? b. In general, what is the required accounting treatment for research and development costs? c. How should goodwill be amortized? they all come together is for question #10arrow_forward

Business Its Legal Ethical & Global EnvironmentAccountingISBN:9781305224414Author:JENNINGSPublisher:Cengage

Business Its Legal Ethical & Global EnvironmentAccountingISBN:9781305224414Author:JENNINGSPublisher:Cengage Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage LearningBusiness/Professional Ethics Directors/Executives...AccountingISBN:9781337485913Author:BROOKSPublisher:Cengage

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage LearningBusiness/Professional Ethics Directors/Executives...AccountingISBN:9781337485913Author:BROOKSPublisher:Cengage