Fundamentals Of Cost Accounting (6th Edition)

6th Edition

ISBN: 9781259969478

Author: WILLIAM LANEN, Shannon Anderson, Michael Maher

Publisher: McGraw Hill Education

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 11, Problem 48E

Net Realizable Value Method

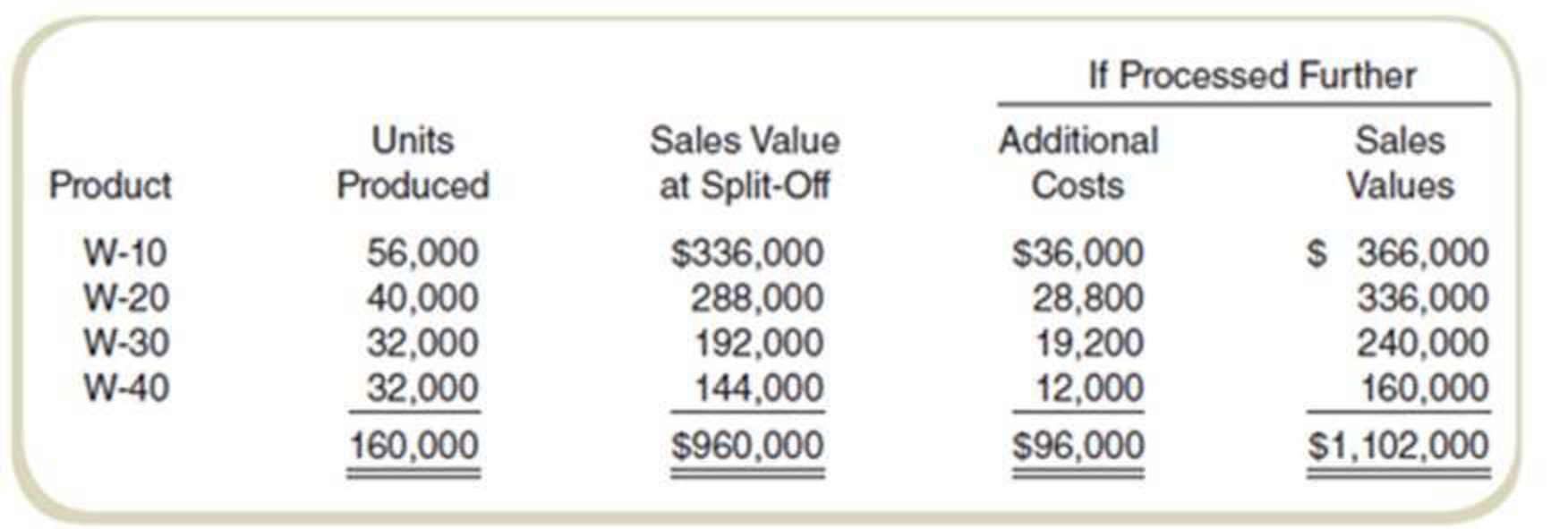

Deming & Sons manufactures four grades of lubricant, W-10, W-20, W-30, and W-40, from a joint process. Additional information follows:

Required

Assuming that total joint costs of $384,000 were allocated using the sales value at split-off (net realizable value method), what joint costs were allocated to each product?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Denver Fabricators manufactures products DF1 and DF2 from a joint process, which also yields a by-product, BP. The company

accounts for the revenues from its by-product sales as other income. Additional information follows:

Units produced

Allocated joint costs

Sales value at split-off

DF1

DF2

BP

DF1

28,700

?

Joint Cost

$573,750

DF2

19,700

?

$191,250

BP

16,700

?

$ 103,700

Total

Required:

Assuming that joint product costs are allocated using the net realizable value at split-off approach, what joint costs are allocated to

each of the joint products DF1 and DF2 and to the by-product, BP?

Note: Do not round intermediate calculations.

65,100

$ 561,700

$ 868,700

Bulldog Canyon Manufacturing produces three products from a joint process. The following information is available

for the period just ended:

Units produced

Joint cost allocation.

Sales value at split-off

Multiple Choice

O

$53,280.

$48,000.

BDC-4

BDC-5

10,800 25,200

$33,120

$57,600.

?

Assume that Bulldog Canyon allocates joint costs using the relative-sales-value method. What is the amount of

joint cost allocation to BDC-4?

$17,280.

$187,200

?

BDC-6

54,000

Not enough information is provided to determine how to allocate the joint cost.

Total

90,000

$144,000

?

2 $468,000

Denver Fabricators manufactures products DF1 and DF2 from a joint process, which also yields a by-product, BP. The company

accounts for the revenues from its by-product sales as other income. Additional information follows:

Units produced

Allocated joint costs

Sales value at split-off

Required:

DF1

28,400

?

$ 571,500

DF2

19,400

?

BP

$ 190,500

16,400

?

$ 103,400

Total

64,200

$ 561,400

$ 865,400

Assuming that joint product costs are allocated using the net realizable value at split-off approach, what joint costs are allocated to

each of the joint products DF1 and DF2 and to the by-product, BP?

Note: Do not round intermediate calculations.

Joint Cost

DF1

DF2

BP

Chapter 11 Solutions

Fundamentals Of Cost Accounting (6th Edition)

Ch. 11 - Why do companies allocate costs? What are some of...Ch. 11 - What are the three methods of allocating service...Ch. 11 - What are the similarities and differences among...Ch. 11 - What criterion should be used to determine the...Ch. 11 - What is a limitation of the direct method of...Ch. 11 - What is a limitation of the step method of...Ch. 11 - Prob. 7RQCh. 11 - Why would a number of accountants express a...Ch. 11 - Prob. 9RQCh. 11 - What is the basic difference between the...

Ch. 11 - Prob. 11RQCh. 11 - If cost allocations arc arbitrary and potentially...Ch. 11 - Prob. 13CADQCh. 11 - Prob. 14CADQCh. 11 - Prob. 15CADQCh. 11 - Prob. 16CADQCh. 11 - Prob. 17CADQCh. 11 - Prob. 18CADQCh. 11 - What are some of the factors that a company needs...Ch. 11 - Prob. 20CADQCh. 11 - Prob. 21CADQCh. 11 - Prob. 22CADQCh. 11 - How is joint cost allocation like service...Ch. 11 - Prob. 24CADQCh. 11 - In what ways is joint cost allocation similar to...Ch. 11 - Why Are Costs Allocated?Ethical Issues You are the...Ch. 11 - Cost Allocation: Direct Method Caro Manufacturing...Ch. 11 - Allocating Service Department Costs First to...Ch. 11 - Cost Allwat ion: Direct Method University Printers...Ch. 11 - Prob. 30ECh. 11 - Cost Allocation: Step Method

Refer to the data for...Ch. 11 - Cost Allocation: Reciprocal Method

Refer to the...Ch. 11 - Cost Allocation: Reciprocal Method, Two Service...Ch. 11 - Cost Allocation: Reciprocal Method

Refer to the...Ch. 11 - Prob. 35ECh. 11 - Prob. 36ECh. 11 - Prob. 37ECh. 11 - Prob. 38ECh. 11 - Prob. 39ECh. 11 - Prob. 40ECh. 11 - Net Realizable Value Method: Multiple Choice

Oak...Ch. 11 - Sell or Process Further: Multiple Choice

Refer to...Ch. 11 - Net Realizable Value Method Euclid Corporation...Ch. 11 - Estimated Net Realizable Value Method Blasto,...Ch. 11 - Net Realizable Value Method to Solve for Unknowns...Ch. 11 - Net Realizable Value Method Bixel Components...Ch. 11 - Net Realizable Value Method with By-Products...Ch. 11 - Net Realizable Value Method Deming Sons...Ch. 11 - Physical Quantities Method

Refer to the facts in...Ch. 11 - Sell or Process Further

Refer to the facts in...Ch. 11 - Physical Quantities Method The following questions...Ch. 11 - Physical Quantities Method; Sell or Process...Ch. 11 - Physical Quantities Method with By-Product...Ch. 11 - Step Method with Three Service Departments Model,...Ch. 11 - Comparison of Allocation Methods BluStar Company...Ch. 11 - Solve for Unknowns: Direct Method Franks Foods has...Ch. 11 - Solve for Unknowns: Step Method RT Renovations is...Ch. 11 - Cost Allocation: Step Method with Analysis and...Ch. 11 - Prob. 59PCh. 11 - Prob. 60PCh. 11 - Direct, Step, and Reciprocal Methods:...Ch. 11 - Cost Allocation: Step and Reciprocal Methods...Ch. 11 - Allocate Service Department Costs: Direct and Step...Ch. 11 - Prob. 64PCh. 11 - Prob. 65PCh. 11 - Prob. 66PCh. 11 - Prob. 67PCh. 11 - Prob. 68PCh. 11 - Fletcher Fabrication, Inc., produces three...Ch. 11 - Findina Missing Data: Net Realizable Value Spartan...Ch. 11 - Finding Missing Data: Net Realizable Value Blaine,...Ch. 11 - Joint Costing in a Process Costing Context:...Ch. 11 - Find Maximum Input Price: Estimated Net Realizable...Ch. 11 - Effect of By-Product versus Joint Cost Accounting...Ch. 11 - Prob. 75PCh. 11 - Prob. 76P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- A company manufactures three products, L-Ten, Triol, and Pioze, from a joint process. Each production run costs 12,900. None of the products can be sold at split-off, but must be processed further. Information on one batch of the three products is as follows: Required: 1. Allocate the joint cost to L-Ten, Triol, and Pioze using the net realizable value method. (Round the percentages to four significant digits. Round all cost allocations to the nearest dollar.) 2. What if it cost 2 to process each gallon of Triol beyond the split-off point? How would that affect the allocation of joint cost to the three products?arrow_forwardNet Realizable Value Method, Decision to Sell at Split-off or Process Further Arvin, Inc., produces two products, ins and outs, in a single process. The joint costs of this process were $60,000, and 13,000 units of ins and 37,000 units of outs were produced. Separable processing costs beyond the split-off point were as follows: ins, $94,000; outs, $465,000. Ins sell for $8.00 per unit; outs sell for $15.00 per unit. Required: 1. Allocate the $60,000 joint costs using the estimated net realizable value method. Ins Outs 2. Suppose that ins could be sold at the split-off point for $7.00 per unit. Should Arvin sell ins at split-off or process them further? Ins Allocated Joint Cost split-off. be processed further as there will be $ less more profit if sold atarrow_forwardBee Dee Fee Company manufactures three products: A, B and C from a joint process. The following information is available for the year 2010: A B C Total Units produced Joint cost allocation Sales value at split-off 12,000 ? 208,000 28,000 36,800 ? 60,000 ? ? 100,000 160,000 520,000 Answer the following: 1. Allocate the joint costs using the Physical Unit Method 2. Allocate the joint costs using the Relative Sales Value Methodarrow_forward

- A company manufactures two joint products at a joint cost of 1,000. These products can be sold at split-off, or when further processed at an additional cost, sold as higher quality items. The decision to sell at split-off or further process should be based on the: A. allocation of the 1,000 joint cost using the quantitative unit measure B. assumption that the 1,000 joint cost is irrelevant C. allocation of the $1,000 joint cost using the relative sales value approach D. assumption that the 1,000 joint cost must be allocated using a physical-measure approach E. allocation of the 1,000 joint cost using any equitable and rational allocation basisarrow_forwardVicerelandu, Inc. manufactures X, Y, and Z from a joint process. Joint product costs were P60,000. Additional information are as follows:(see pic) 1. Assuming that joint costs are allocated using the physical measures (units produced) approach, what were the total costs allocated to product X ________________________ Y ______________________ Z ______________________2. Assuming that joint product costs are allocated using the relative sales value at split-off approach, what were the total costs allocated to product X_________________________ y ______________________ Z ______________________arrow_forwardAfter allocating the joint process costs to its two joint products, Allomar Co. reports gross margin percentages of 30% for Product A and 40% for Product B. Sales reported for each product were $25,000 for Product A and $60,000 for Product B. Neither of the two products were processed beyond the split-off point. Calculate the total amount of joint costs assigned between the two products. Allocated joint costs Product A Product B Assuming Allomar used the physical quantities method to allocate the joint costs, what percentage of the total production volume did Product B represent? (Round answer to 2 decimal places, e.g. 15.25%.) Proportion of joint costs assigned to product B %arrow_forward

- Net Realizable Value Method, Decision to Sell at Split-off or Process Further Arvin, Inc., produces two products, ins and outs, in a single process. The joint costs of this process were $60,000, and 14,000 units of ins and 36,000 units of outs were produced. Separable processing costs beyond the split-off point were as follows: ins, $102,000; outs, $450,000. Ins sell for $8.00 per unit; outs sell for $15.00 per unit. Required: 1. Allocate the $60,000 joint costs using the estimated net realizable value method. Allocated Joint Cost Ins $fill in the blank 1 Outs $fill in the blank 2 2. Suppose that ins could be sold at the split-off point for $7.00 per unit. Should Arvin sell ins at split-off or process them further?Ins be processed further as there will be $fill in the blank 4 profit if sold at split-off.arrow_forwardNet Realizable Value Method, Decision to Sell at Split-off or Process Further Pacheco, Inc., produces two products, overs and unders, in a single process. The joint costs of this process were $60,000, and 14,000 units of overs and 36,000 units of unders were produced. Separable processing costs beyond the split-off point were as follows: overs, $18,000; unders, $23,040. Overs sell for $2.00 per unit; unders sell for $3.14 per unit. Required: 1. Allocate the $60,000 joint costs using the estimated net realizable value method. Allocated Joint Cost Overs Unders 2. Suppose that overs could be sold at the split-off point for $1.80 per unit. Should Pacheco sell overs at split-off or process them further? Overs be processed further as there will be $ profit if sold at split-off.arrow_forwardNet Realizable Value Method, Decision to Sell at Split-off or Process Further Arvin, Inc., produces two products, ins and outs, in a single process. The joint costs of this process were $50,000, and 15,000 units of ins and 36,000 units of outs were produced. Separable processing costs beyond the split-off point were as follows: ins, $110,000; outs, $450,000. Ins sell for $8.00 per unit; outs sell for $15.00 per unit. Required: 1. Allocate the $50,000 joint costs using the estimated net realizable value method. Ins Outs Allocated Joint Cost 2. Suppose that ins could be sold at the split-off point for $7.00 per unit. Should Arvin sell ins at split-off or process them further? profit if sold at split-off. Ins be processed further as there will be $arrow_forward

- Tango Company produces joint products M, N, and T from a joint process. This information concerns a batch produced in April at a joint cost of $165,000: Product M N Product M Units Produced and Sold 14,500 N T 8,500 9,500 After Split-Off Allocated Joint Cost Total Separable Costs $ 13,900 13,400 6,700 Required: How much of the joint cost should be allocated to each joint product using the net realizable value method? (Do not round intermediate calculations. Enter your final answers in whole dollars.) Total Final Sales Value $ 205,000 185,000 34,000arrow_forwardJoint Cost Allocation—Weighted Average Method Custom Carvings Company jointly produces wood chips and sawdust used in agriculture. The wood chips and sawdust are actually by-products of the company’s core operations, but Custom Carvings accounts for them just like normally produced goods because of their large volumes. One jointly produced batch yields 2,000 cubic yards of wood chips and 6,000 cubic yards of sawdust, and the estimated cost per batch is $27,300. However, the joint production of each good is not equally weighted. Given management estimates for how long it takes to make sawdust vs. wood chips, a weight factor of 14 is used for wood chips in the joint production process, and a weight factor of 2 is used for sawdust. Given this information, allocate the joint costs of production to each product using the weighted average method. Joint Product Allocation Sawdust Wood chips Totalsarrow_forwardJoint Cost Allocation—Weighted Average Method Custom Carvings Company jointly produces wood chips and sawdust used in agriculture. The wood chips and sawdust are actually by-products of the company’s core operations, but Custom Carvings accounts for them just like normally produced goods because of their large volumes. One jointly produced batch yields 2,000 cubic yards of wood chips and 6,000 cubic yards of sawdust, and the estimated cost per batch is $27,300. However, the joint production of each good is not equally weighted. Given management estimates for how long it takes to make sawdust vs. wood chips, a weight factor of 14 is used for wood chips in the joint production process, and a weight factor of 2 is used for sawdust. Given this information, allocate the joint costs of production to each product using the weighted average method. Joint Product Allocation Sawdust $fill in the blank 1 Wood chips fill in the blank 2 Totals $fill in the blank 3arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Incremental Analysis - Sell or Process Further; Author: Melissa Shirah;https://www.youtube.com/watch?v=7D6QnBt5KPk;License: Standard Youtube License