Fundamentals Of Cost Accounting (6th Edition)

6th Edition

ISBN: 9781259969478

Author: WILLIAM LANEN, Shannon Anderson, Michael Maher

Publisher: McGraw Hill Education

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 11, Problem 62P

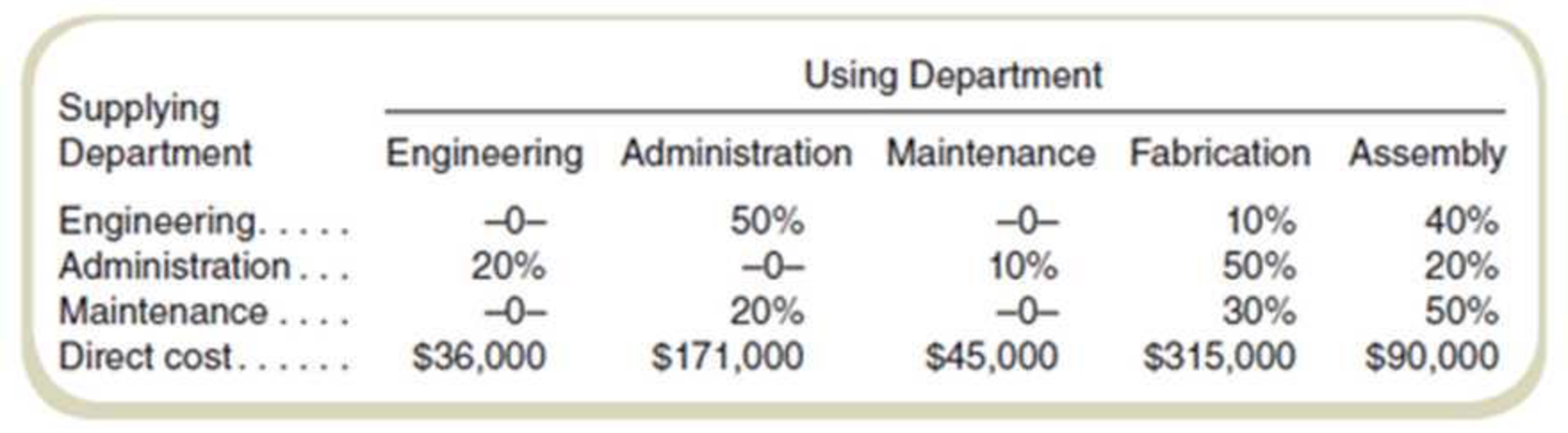

Cost Allocation: Step and Reciprocal Methods

Midland Resources has two production departments (Fabrication and Assembly) and three service departments (Engineering. Administration, and Maintenance). During July, the following costs and service department usage ratios were recorded:

Required

Allocate the service department costs to the two operating departments using the reciprocal method. (Hint: You do not need to use a computer or study the Appendix in this chapter.)

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Step-Down Method

The Ferre Publishing Company has three service departments and two operating departments. Selected data from a recent period on the five departments follow

The company allocates service department costs by the step-down method in the following order: Administration (number of employees). Janitorial (space occupied), and Maintenance (hours of press time).

Required:

Using the step-down method, allocate the service department costs to the operating departments.:

AI Rawabi company consist of two support departments (Administration and R& D) and two operating departments

(Manufacturing & Assembling). The cost of Administration department is allocated based on number of employees and the cost

of R& D department is allocated based on research hours. The table below shows the cost details. Allocate the cost of the

support departments to the operating departments using step-down method. How much is the Assembling department total

cost after cost allocation:

Support Departments

Operating Departments

R&D Manufacturing Assembling Total Cost

Admin

Cost:

Salaries

30000

60000

44000

70000

204000

Supplies

10000

30000

25000

30000

95000

Total

40000

90000

69000

100000

299000

Allocation Base:

Research Hours

200

300

450

250

Number of Employees

7

10

9

13

Select one:

O a. RO 155775

O b. RO 162090.3

O c. RO 143225

O d. 136909.7

An activity based costing system is being considered at Evelia, nv to assign products overhead costs; these overhead costs are currently assigned strictly by number of units produced. First, the two overhead costs of Rent expense and Insurance expense would be allocated to three activity cost pools - Finishing, Sanding, and Other - based on resource consumption. The information used to perform these allocations is below:

Overhead Costs:

Rent expense: $2,000,000

Insurance expense: $1,650,000

Distribution of Resource Consumption across Activity Cost Pools:

Overhead Cost

Activity Cost Pools

Finishing

Sanding

Other

Rent expense

0.45

0.25

0.30

Insurance expense

0.20

0.35

0.45

In the second stage, Finishing costs would be assigned to products using direct labor hours and Sanding costs would be assigned to products using the number of machine hours. The costs in the Other activity pool would not be assigned to products. Activity data for the company's two products is as…

Chapter 11 Solutions

Fundamentals Of Cost Accounting (6th Edition)

Ch. 11 - Why do companies allocate costs? What are some of...Ch. 11 - What are the three methods of allocating service...Ch. 11 - What are the similarities and differences among...Ch. 11 - What criterion should be used to determine the...Ch. 11 - What is a limitation of the direct method of...Ch. 11 - What is a limitation of the step method of...Ch. 11 - Prob. 7RQCh. 11 - Why would a number of accountants express a...Ch. 11 - Prob. 9RQCh. 11 - What is the basic difference between the...

Ch. 11 - Prob. 11RQCh. 11 - If cost allocations arc arbitrary and potentially...Ch. 11 - Prob. 13CADQCh. 11 - Prob. 14CADQCh. 11 - Prob. 15CADQCh. 11 - Prob. 16CADQCh. 11 - Prob. 17CADQCh. 11 - Prob. 18CADQCh. 11 - What are some of the factors that a company needs...Ch. 11 - Prob. 20CADQCh. 11 - Prob. 21CADQCh. 11 - Prob. 22CADQCh. 11 - How is joint cost allocation like service...Ch. 11 - Prob. 24CADQCh. 11 - In what ways is joint cost allocation similar to...Ch. 11 - Why Are Costs Allocated?Ethical Issues You are the...Ch. 11 - Cost Allocation: Direct Method Caro Manufacturing...Ch. 11 - Allocating Service Department Costs First to...Ch. 11 - Cost Allwat ion: Direct Method University Printers...Ch. 11 - Prob. 30ECh. 11 - Cost Allocation: Step Method

Refer to the data for...Ch. 11 - Cost Allocation: Reciprocal Method

Refer to the...Ch. 11 - Cost Allocation: Reciprocal Method, Two Service...Ch. 11 - Cost Allocation: Reciprocal Method

Refer to the...Ch. 11 - Prob. 35ECh. 11 - Prob. 36ECh. 11 - Prob. 37ECh. 11 - Prob. 38ECh. 11 - Prob. 39ECh. 11 - Prob. 40ECh. 11 - Net Realizable Value Method: Multiple Choice

Oak...Ch. 11 - Sell or Process Further: Multiple Choice

Refer to...Ch. 11 - Net Realizable Value Method Euclid Corporation...Ch. 11 - Estimated Net Realizable Value Method Blasto,...Ch. 11 - Net Realizable Value Method to Solve for Unknowns...Ch. 11 - Net Realizable Value Method Bixel Components...Ch. 11 - Net Realizable Value Method with By-Products...Ch. 11 - Net Realizable Value Method Deming Sons...Ch. 11 - Physical Quantities Method

Refer to the facts in...Ch. 11 - Sell or Process Further

Refer to the facts in...Ch. 11 - Physical Quantities Method The following questions...Ch. 11 - Physical Quantities Method; Sell or Process...Ch. 11 - Physical Quantities Method with By-Product...Ch. 11 - Step Method with Three Service Departments Model,...Ch. 11 - Comparison of Allocation Methods BluStar Company...Ch. 11 - Solve for Unknowns: Direct Method Franks Foods has...Ch. 11 - Solve for Unknowns: Step Method RT Renovations is...Ch. 11 - Cost Allocation: Step Method with Analysis and...Ch. 11 - Prob. 59PCh. 11 - Prob. 60PCh. 11 - Direct, Step, and Reciprocal Methods:...Ch. 11 - Cost Allocation: Step and Reciprocal Methods...Ch. 11 - Allocate Service Department Costs: Direct and Step...Ch. 11 - Prob. 64PCh. 11 - Prob. 65PCh. 11 - Prob. 66PCh. 11 - Prob. 67PCh. 11 - Prob. 68PCh. 11 - Fletcher Fabrication, Inc., produces three...Ch. 11 - Findina Missing Data: Net Realizable Value Spartan...Ch. 11 - Finding Missing Data: Net Realizable Value Blaine,...Ch. 11 - Joint Costing in a Process Costing Context:...Ch. 11 - Find Maximum Input Price: Estimated Net Realizable...Ch. 11 - Effect of By-Product versus Joint Cost Accounting...Ch. 11 - Prob. 75PCh. 11 - Prob. 76P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- A manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardA manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardExercise 11-29 (Algo) Cost Allocation: Direct Method (LO 11-2) University Printers has two service departments (Maintenance and Personnel) and two operating departments (Printing and Developing). Management has decided to allocate maintenance costs on the basis of machine-hours in each department and personnel costs on the basis of labor-hours worked by the employees in each. The following data appear in the company records for the current period: Maintenance Personnel Printing Developing Machine-hours — 1,800 1,800 4,200 Labor-hours 550 — 550 2,200 Department direct costs $ 2,000 $ 12,000 $ 13,600 $ 10,500 Required: Use the direct method to allocate these service department costs to the operating departments. (Negative amounts should be indicated by a minus sign. Do not round intermediate calculations.) Maintenance Personnel Printing Developing Service department costs Maintenance allocation…arrow_forward

- Exercise 11-29 (Algo) Cost Allocation: Direct Method (LO 11-2) University Printers has two service departments (Maintenance and Personnel) and two operating departments (Printing and Developing). Management has decided to allocate maintenance costs on the basis of machine-hours in each department and personnel costs on the basis of labor-hours worked by the employees in each. The following data appear in the company records for the current period: Maintenance Personnel Printing Developing Machine-hours — 1,700 1,700 5,100 Labor-hours 500 — 500 3,500 Department direct costs $ 3,000 $ 13,000 $ 14,100 $ 11,200 Required: Use the direct method to allocate these service department costs to the operating departments. (Negative amounts should be indicated by a minus sign. Do not round intermediate calculations.)arrow_forwardComparison of Methods of Allocation Duweynie Pottery, Inc., is divided into two operating divisions: Pottery and Retail. The company allocates Power and General Factory department costs to each operating division. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data: Use the rounded values for subsequent calculations. Support Departments Operating Divisions Power General Factory Pottery Retail Overhead costs $140,400 $190,800 $96,000 $56,000 Machine hours 2,000 2,500 7,000 3,000 Square footage 2,500 1,700 4,000 6,000 Round all allocation ratios to four significant digits. Round all allocated amounts to the nearest dollar. Required: 3. Allocate the support service costs using the reciprocal method. Note: If…arrow_forwardComparison of Methods of Allocation Duweynie Pottery, Inc., is divided into two operating divisions: Pottery and Retail. The company allocates Power and General Factory department costs to each operating division. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data: Use the rounded values for subsequent calculations. Support Departments Operating Divisions Power General Factory Pottery Retail Overhead costs $150,000 $171,600 $97,000 $55,000 Machine hours 2,000 2,500 7,000 3,000 Square footage 2,500 1,700 4,000 6,000 Round all allocation ratios to four significant digits. Round all allocated amounts to the nearest dollar. Required: 3. Allocate the support service costs using the reciprocal method. Note: If…arrow_forward

- Comparison of Methods of Allocation Duweynie Pottery, Inc., is divided into two operating divisions: Pottery and Retail. The company allocates Power and General Factory department costs to each operating division. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data: Use the rounded values for subsequent calculations. Support Departments Operating Divisions Pottery Retail Power $140,400 Overhead costs $99,000 $57,000 Machine hours 2,000 7,000 3,000 Square footage 2,500 4,000 6,000 Round all allocation ratios to four significant digits. Round all allocated amounts to the nearest dollar. Required: 1. Allocate the support service costs using the direct method. Note: Input to two decimal places. Allocation Ratios Proportion of machine hours Proportion of…arrow_forwardWoodstock Binding has two service departments, IT (Information Technology) and HR (Human Resources), and two operating departments, Publishing and Binding. Management has decided to allocate IT costs on the basis of IT Tickets (issued with each IT request) in each department and HR costs on the basis of employees in each department. The following data appear in the company records for the current period: IT tickets Employees Department direct costs a. The order of allocation starts with IT. b. The order of allocation starts with HR. IT Required A HR 1,200 0 0 16 $ 152,000 $ 249,600 Required: Use the step method to allocate the service costs, using the following: Required B Publishing 1,200 24 $430,000 Complete this question by entering your answers in the tabs below. X Answer is not complete. Use the step method to allocate the service costs, using the following: Binding Return to question 3,600 40 $ 390,000arrow_forwardStep-Down Method Madison Park Co-op, a whole foods grocery and gift shop, has provided the following data to be used in its service department cost allocations: Required: Using the step-down method, allocate the costs of the service departments to the two operating departments. Allocate Administration first on the basis of employee-hours and then Janitorial on the basis of space occupied.arrow_forward

- Direct Method Seattle Western University has provided the following data to be used in its service department cost allocations: Required: Using the direct method, allocate the costs of the service departments to the two operating departments. Allocate the Administration cost on the basis of student credit-hours and the Facility Services cost on the basis of space occupied.arrow_forwardSupport-department cost allocations; direct, step-down, and reciprocal methods. Ballantine Corporation has two operating departments: Eastern Department and Western Department. Each of the operating departments uses the services of the company’s two support departments: Engineering and Information Technology. Additionally, the Engineering and Information Technology departments use the services of each other. Data concerning the past year are as follows:arrow_forwardWoodstock Binding has two service departments, IT (Information Technology) and HR (Human Resources), and two operating departments, Publishing and Binding. Management has decided to allocate IT costs on the basis of IT Tickets (issued with each IT request) in each department and HR costs on the basis of employees in each department. The following data appear in the company records for the current period: IT tickets Employees Department direct costs Service department costs IT allocation HR allocation Total costs allocated $ IT IT 0 25 $ 159,000 Required: Use the direct method to allocate these service department costs to the operating departments. Note: Amounts to be deducted should be indicated by a minus sign. Do not round intermediate calculations. Round "Publishing" and "Binding" answers to 2 decimal places. HR 1,100 0 $ 247,500 0 $ HR Publishing 1,100 33 $ 430,000 0 $ Publishing Binding 3,300 49 $ 390,000 0.00 $ Binding 0.00arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

What is Cost Allocation? Definition & Process; Author: FloQast;https://www.youtube.com/watch?v=hLhvvHvZ3JM;License: Standard Youtube License