Videos

Western States Supply, Inc. (WSS), consists of three divisions—California, Northwest, and Southwest—that operate as if they were independent companies. Each division has its own sales force and production facilities. Each division manager is responsible for sales, cost of operations, acquisition and financing of divisional assets, and

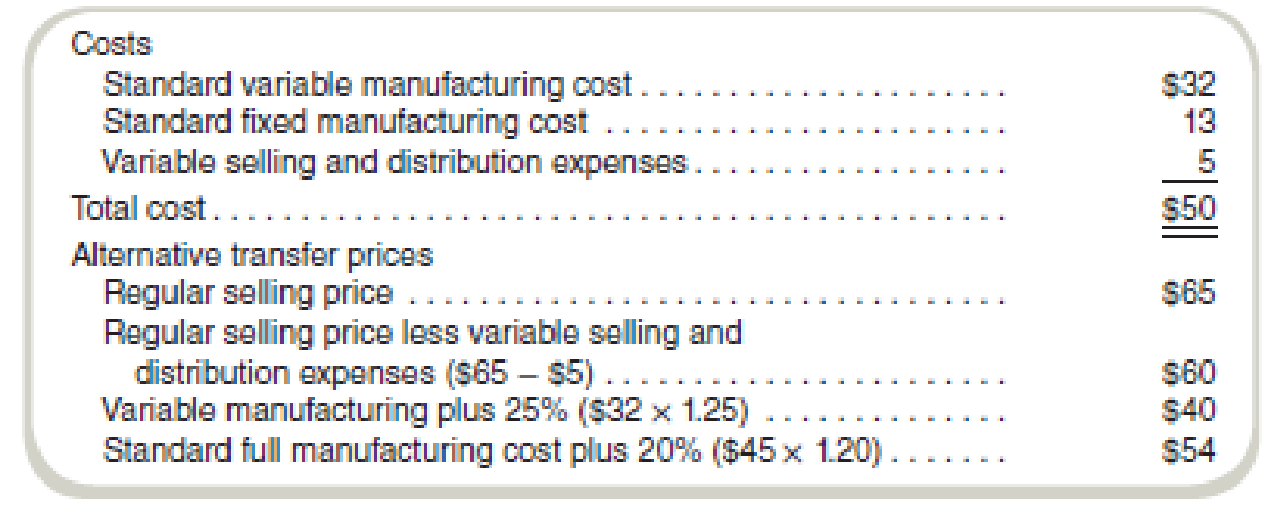

Southwest has just been awarded a contract for a product that uses a component manufactured by outside suppliers as well as by Northwest, which is operating well below capacity. Southwest used a cost figure of $37 for the component in preparing its bid for the new product. Northwest supplied this cost figure in response to Southwest’s request for the

Northwest’s regular selling price for the component that Southwest needs is $65. Northwest’s management indicated that it could supply Southwest the required quantities of the component at the regular selling price less variable selling and distribution expenses. Southwest management responded by offering to pay standard variable manufacturing cost plus 25 percent.

The two divisions have been unable to agree on a transfer price. Corporate management has never established a transfer price policy. The corporate controller suggested a price equal to the standard full manufacturing cost (that is, no selling and distribution expenses) plus a 20 percent markup. The two division managers rejected this price because each considered it grossly unfair.

The unit cost structure for the Northwest component and the suggested prices follow

Required

- a. Discuss the effect that each of the proposed prices could have on the attitude of Northwest’s management toward intracompany business.

- b. Is the negotiation of a price between Northwest and Southwest a satisfactory method to solve the transfer price problem? Explain your answer.

- c. Should WSS’s corporate management become involved in this transfer price controversy? Explain your answer.

Want to see the full answer?

Check out a sample textbook solution

Chapter 15 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Elba Consulting Associates (ECA) is organized into three divisions (Manufacturing, Retail, and Entertainment). Many support services, such as human resources, legal, and information technology, are provided by corporate staff. The corporate staff costs are allocated to the divisions based on divisional revenue. The resulting divisional operating profit (computed as divisional revenues less divisional direct costs less corporate cost allocations) is used to evaluate and compensate all division managers. The compensation plan consists of a fixed salary plus a bonus, which depends on the actual divisional operating profit compared to the target profit. The fixed salary for all three division managers is $500,000. The bonus consists of two parts. First, there is a "target bonus," which is a flat $25,000 for meeting the operating profit target. Second, there is an "incentive bonus," which is equal to 0.2% of salary for every thousand dollars of operating profit in excess of the target. The…arrow_forwardCorcoran Heavy Industries Company (CHIC) is organized into four divisions, each of which operates in a different industry. The types of customer served and the method used to distribute products differ across all four of these industries. In addition, each division must comply with its own unique set of industry regulations related to issues such as safety and recyclability of materials.Operating profit before depreciation and amortization is the measure of profit regularly used by the chief operating decision maker for evaluating the performance of each of these divisions. In addition, information for each division on capital expenditures and depreciation and amortization is routinely provided by corporate headquarters to the chief operating decision maker. A summary of the information provided to the chief operating decision maker at the end of the current year is as follows:Required I. Prepare a report for CHIC's management evaluating whether the operating segments disclosures…arrow_forwardGoodworks Software operates stores within five regions. Regional managers are held accountable for marketing, advertising, and sales decisions, and all costs incurred within their region. In addition, regional managers decide whether new stores will open, where the stores will be located, and whether the stores will lease or purchase the facilities. Store managers, in contrast, are accountable for marketing, advertising, and sales decisions, and costs incurred within their stores. Ideally, on the basis of this information, what type of responsibility center should the software company use to evaluate its regions and stores? (1) Regions; (2) Stores (1) Profit center; (2) Profit center (1) Profit center; (2) Revenue center (1) Investment center; (2) Cost center (1) Investment center; (2) Profit center (1) Profit center; (2) Cost centerarrow_forward

- Raddington Industries produces tool and die machinery for manufacturers. The company expanded vertically in 20x1 by acquiring one of its suppliers of alloy steel plates, Keimer Steel Company. To manage the two separate businesses, the operations of Keimer are reported separately as an investment center. Raddington monitors its divisions on the basis of both unit contribution and return on average investment (ROI), with investment defined as average operating assets employed. Management bonuses are determined on ROI. All investments in operating assets are expected to earn a minimum return of 13 percent before income taxes. Keimer's cost of goods sold is considered to be entirely variable, while the division's administrative expenses are not dependent on volume. Selling expenses are a mixed cost with 40 percent attributed to sales volume. Keimercontemplated a capital acquisition with an estimated ROI of 14.5 percent;however, division management decided against the investment because…arrow_forwardXerox Corporation has been an innovator in its responsibility-accounting system. In one initiative, management changed the responsibility-center orientation of its Logistics and Distribution Department from a cost center to a profit center. The department manages the inventories and provides other logistical services to the company s Business Systems Group. Formerly, the manager of the Logistics and Distribution Department was held accountable for adherence to an operating expense budget. Now the department "sells" its services to the company s other segments, and the department s manager is evaluated partially on the basis of the department s profit. Xerox Corporation s management feels that the change has been beneficial. The change has resulted in more innovative thinking in the department and has moved decision making down to lower levels in the company. Required: Comment on the new responsibility-center designation for the Logistics and Distribution Department.arrow_forwardYou firm has just been hired by Toes in the Water, Inc., a manufacturer of kayaks, to provide consulting services. Toes in the Water operates two divisions: Ocean and Lake. Each divisional vice president is held responsible for both profit and invested capital. Each division consists of two branches: Sand and Clay. Each branch manager is responsible for generating revenue and controlling costs. The Ocean division's Sand branch has two departments, Zac and Brown. Both department managers are responsible for controlling costs. You asked a staff member to provide a list of the performance evaulation tools they would suggest using to evaluate the Sand and Clay branches. They provided the following list: budget versus actual report • segmented income statement • return on investment Do you agree with the staff member's list? Why or why not? A. No. Return on investment should not be used because the branches are considered profit centers. B. Yes. All of the tools listed are valid performance…arrow_forward

- Cable Network System Bhd (CNS) is a supplier of equipment to telecommunication companies such as Maxis, Celcom and Astro. It has two division, Component Division and the Equipment Division. CNS adopts a decentralized management system where managers are essentially free to determine whether goods will be transferred internally and what would be the internal transfer prices. CNS policy is that for all internal transfers between divisions, the transfer price be expressed on a full cost basis. The markup in the full cost arrangement is left to the discretion of divisional managers. The managers of the two division held a meeting to discuss on the pricing arrangement for a mini- antennae produced by the component division. Production of the mini-antennae is currently at full capacity. The Component Division can sell the mini-antennae for RM 46.50 to outside customers. The Equipment Division can also buy the mini-antennae from external sources for the same price. The manager of the…arrow_forwardCable Network System Bhd (CNS) is a supplier of equipment to telecommunication companies such as Maxis, Celcom and Astro. It has two division, Component Division and the Equipment Division. CNS adopts a decentralized management system where managers are essentially free to determine whether goods will be transferred internally and what would be the internal transfer prices. CNS policy is that for all internal transfers between divisions, the transfer price be expressed on a full cost basis. The markup in the full cost arrangement is left to the discretion of divisional managers. The managers of the two division held a meeting to discuss on the pricing arrangement for a mini- antennae produced by the component division. Production of the mini-antennae is currently at full capacity. The Component Division can sell the mini-antennae for RM 46.50 to outside customers. The Equipment Division can also buy the mini-antennae from external sources for the same price. The manager of the…arrow_forwardThe Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forward

- The Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forwardThe Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forwardXerox Corporation has been an innovator in its responsibility-accounting system. In one initiative, management changed the responsibility-centre orientation of its Logistics and Distribution Department from a cost centre to a profit The department manages the inventories and provides other logistical services to the company’s Business Systems Group. Formerly, the manager of the Logistics and Distribution Department was held accountable for adherence to an operating expense budget. Now the department “sells” its services to the company’s other segments, and the department’s manager is evaluated partially on the basis of the department’s profit. Xerox Corporation’s management feels that the change has been beneficial. The change has resulted in more innovative thinking in the development and has moved decision making down to lower levels in the company. Required: Comment on the new responsibility-centre designation for the Logistics and Distribution Department.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub